というNBER論文が上がっている。原題は「Tariffs as Cost-Push Shocks: Implications for Optimal Monetary Policy」で、著者はIván Werning(MIT)、Guido Lorenzoni(シカゴ大)、Veronica Guerrieri(同)。

以下はその要旨。

We study the optimal monetary policy response to the imposition of tariffs in a model with imported intermediate inputs. In a simple open-economy framework, we show that a tariff maps exactly into a cost-push shock in the standard closed-economy New Keynesian model, shifting the Phillips curve upward. We then characterize optimal monetary policy, showing that it partially accommodates the shock to smooth the transition to a more distorted long-run equilibrium—at the cost of higher short-run inflation.

(拙訳)

我々は、輸入中間財のあるモデルで、関税が課されたことへの最適な金融政策の反応を調べた。単純な開放経済の枠組みで我々は、関税が標準的な閉鎖経済ニューケインジアンモデルにおけるコストプッシュショックにまさに対応し、フィリップス曲線を上方にシフトすることを示す。次いで我々は最適な金融政策の特性を求め、より歪みのある長期の均衡への移行を平滑化するために、そうした政策が短期のインフレ上昇を対価として部分的にショックを受容することを示す。

以下は著者の一人(Werning)による論文の解説連ツイ。

What should the Fed do with Trump Tariffs?

New paper on 'Monetary Policy in Times of Tariffs' with Guido Lorenzoni & Veronica Guerrieri (link at end)

We show the simplest most intuitive way to approach tariffs is actually correct:

Tariffs = textbook cost-push shock

🧵1/N

The Fed recently hit the pause button on adjusting rates due to tariffs. A month ago Fed Chair Powell said:

“We may find ourselves in the challenging scenario in which our dual-mandate goals are in tension.” (Speech at Economic Club of Chicago, April 16)

2/N

Our main result: In a simple open-economy model with imported intermediates, a tariff acts AS IF it were a labor wedge in a standard New Keynesian closed economy.

The good: standard results & insights on cost-push shocks directly apply!

The bad: cost push shocks are bad!

3/N

Intuitively, as Powell said, tariffs raise costs and lower productivity. They are a negative supply shock that creates a nastier tradeoff for the dual mandate.

Very intuitive... but international macro models are more involved.

Our result formalizes the simple intuition. 4/N

Translation: Tariffs shift the Phillips curve up.

The central bank faces a tradeoff: control inflation or support output.

It can’t do both.

So what should monetary policy do?... 5/N

We analytically characterize the optimal response.

Spoiler: it involves tolerating inflation—temporarily.

It involves softening the blow of tariffs on output and labor.

Intuitively ....

Intuition: tariffs lower the natural real wage (due to lower profitability) more than productivity. This creates a positive labor wedge, which drives the cost-push effect.

In fact, technically: the productivity loss is second-order, but profitability loss is first order.

It looks something like this using a basic microeconomic intuition. The economy frontier goes down, but also wages are not equal to actual productivity, they are lower, so labor is distorted down. The second effect is stronger starting from free trade.

So tariffs are bad, can lead to sharp hit. Optimal monetary policy smooths the adjustment...

Inflation rises in the short run

Output stays above the distorted steady state

Gradual convergence to lower level follows

6/N

Technically, our AS IF result is as follows.

- an extra "cost push" epsilon term in the Phillips curve, so it is pushes the curve out.

- the welfare objective is unchanged: dual mandate penalizing inflation and output deviations.

7/N

Basically, you can do open economy macro with your closed economy model.

Here are some numerical examples run thro the model...

Here’s what’s NOT optimal...

1. Targeting zero inflation. That would require a sharp contraction in output—too costly.

Letting inflation run a bit helps cushion the blow.

2. "See through principle": hoping inflation rises, but minimally, via direct costs. 9/N

The results hold with sticky wages, but then inflation control is even costlier.

Zero inflation now requires deeper recessions and wage deflation.

The optimal policy is still to accommodate—with some inflation.

A common idea in policy circles is the "see through principle" (not really grounded in economic theory).

It makes some sense as a simple communication device or slogan, but our model says...

... optimal inflation typically exceeds the mechanical pass-through from tariffs.

The effects show up in the nominal exchange rate too...

In our setup, tariffs raise prices and depreciate the currency.

This echoes recent empirical patterns during trade tensions.

(capital flight is surely another reason, but basic macro+trade can already explain it)

Lots of policy commentary says “central banks shouldn’t respond to tariffs.”

That’s not what our model says.

A better rule: Don’t overreact, but don’t ignore either.

Bottom line...

Tariffs create inflation-output tradeoffs that monetary policy can’t ignore.

Our equivalence result gives a simple way to map these shocks onto classic macro models—and solve them analytically

In the process justifying simple intuitions that serve as guiding lines. It's important to check and ground good intuitions!

Hope this adds some clarity to the tariff debates.

Thanks for reading!

Paper here...

Adding an alternative non-NBER link in case anyone had issues with that:

https://economics.mit.edu/sites/default/files/inline-files/tariff%20MP%20draft.pdf

My coauthors: @guido_lorenzoni @VeronicaGuerri7

Shout out to other recent research on this topic, referenced in the paper

@JavierBianchi7 @a_auclert @ludwigstraub @monacelt @skalemliozcan @FabioGhironi

(拙訳)

FRBはトランプ関税にどう対応すべきか?

グイド・ロレンツォーニ、ベロニカ・グエリエリと共著した「関税の時代における金融政策」に関する新たな論文(リンクは最後に)。

我々は、関税にアプローチする最も単純で直観的なやり方が実際に正しいことを示す:

関税=教科書のコストプッシュショック

最近、関税のせいでFRBは金利調整の一時停止ボタンを押した。1か月前、パウエルFRB議長はこう述べた:

「我々の2つの責務の目標に圧力が掛かる難しいシナリオに我々はいるのかもしれない(シカゴ経済クラブでの4月16日講演*1)」

我々の主要な結果:輸入中間財のある単純な開放経済モデルでは、関税は標準的なニューケインジアン閉鎖経済モデルにおける労働ウェッジ*2のように働く。

良い点:コストプッシュショックに関する標準的な結果と洞察が直接的に適用できる!

悪い点:コストプッシュショックは悪いものである!

直観的には、パウエルが言ったように、関税は費用を高め生産性を低める。それは、2つの責務のトレードオフをより厄介なものとする負の供給ショックである。

非常に直観的な話だ・・・だが、国際マクロモデルはもっと複雑なものである。

我々の結果は単純な直観を定式化する。

翻訳:関税はフィリップス曲線を上方にシフトさせる。

中銀はトレードオフに直面する:インフレを制御するか、もしくは生産を支援するか。

両方はできない。

では、金融政策はどうすべきか?

我々は最適な反応を解析的に特徴付けた。

ネタばれ:インフレを――一時的に――許容することになる。

関税の生産と労働への打撃を緩和することになる。

直観的には・・・

直観:関税は(利益率低下により)自然実質賃金を生産性よりも大きく低下させる。これは正の労働ウェッジを生み出し、それがコストプッシュ効果をもたらす。

実際のところ、技術的には、生産性の損失は2次的なものであり、利益率の損失が1次的なものである。

基本的なマクロ経済学の直観を用いると以下の図のようになる。経済のフロンティアは下に下がるが、賃金は実際の生産性に等しくなくなるためさらに下がり、労働は歪んだ形で低下する。自由貿易を出発点とすると、2番目の効果の方が強くなる。

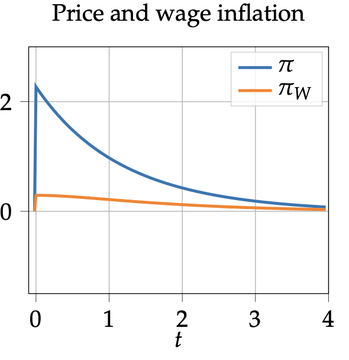

ということで関税は悪いものであり、厳しい打撃をもたらし得る。最適金融政策は調整を平滑化する・・・

インフレは短期的に上昇する

生産は歪んだ定常状態より上に維持される

より低い水準への段階的な収束がその後生じる技術的には、我々の「かのように」の結果は次の通りである。

基本的に、閉鎖経済モデルで開放経済マクロを行うことができる。

以下はモデルを走らせた数値例である・・・

以下は最適ではないこと・・・

- ゼロインフレ目標。それは生産の急激な縮小を必要とする――あまりにも高く付く。

インフレを少し高くすることが打撃を和らげる助けとなる。- 「注視原則」:インフレが直接的費用により最小限だけ上昇すると期待すること。

今回の結果は粘着的な賃金についても当てはまるが、インフレ制御のコストは一層高くなる。

その場合、ゼロインフレはより深刻な不況と賃金デフレを必要とする。

最適政策は依然として緩和的なものであるが、幾ばくかのインフレを伴う。

政策界隈での一般的な考え方は、「注視原則」である(実際の経済理論に基づいたものではない)*3。

単純なコミュニケーションツールもしくはスローガンとしては幾らかの意味はあるが、我々のモデルによれば、・・・

・・・最適インフレは関税の機械的な転嫁分を上回るのが普通である。関税の効果は名目為替相場にも表れる・・・

我々の枠組みでは、関税は物価を上昇させて通貨を減価させる。

これは、最近の貿易紛争における実証結果のパターンに沿うものである。

(キャピタルフライトもその一つの要因になるのは確かだが、基本的なマクロ+貿易だけで説明できるのである)

多くの政策解説者は「中銀は関税に反応すべきではない」と言う。

我々のモデルはそれとは違う結果を出している。

もっと良いルールは、過剰反応するな、ただし無視もするな、というものだ。

要点は・・・

関税はインフレと生産のトレードオフをもたらし、金融政策はそれを無視できない。

我々の同等性の結果は、そうしたショックを古典的なマクロモデルに移し替えて、解析的に解く単純な方法を提示する。

その過程で、指針として使われる単純な直観が正当化される。良い直観をチェックし基礎とするのは重要なことなのだ!

この結果が関税に関する議論を幾らか明確にすることを望む。

読んでくれたことに感謝!

論文はこちら・・・*4

そちらでは問題がある人のため、NBERではない別リンクを追加しておく。

https://economics.mit.edu/sites/default/files/inline-files/tariff%20MP%20draft.pdf

共著者は@guido_lorenzoni @VeronicaGuerri7

論文で参照したこのトピックに関する最近の研究者にもメンションしておく。

@JavierBianchi7 @a_auclert @ludwigstraub @monacelt @skalemliozcan @FabioGhironi

この連ツイに対して、モデルでは関税が恒久的であることを仮定しているのか、関税が廃止される可能性があれば結論は変わるのか、というレスが付いており、それに対しWerningは、それが我々のベースラインだ(150%ではなく20%)、ただコストプッシュの等価性に関する我々の結果はもっと幅広くあてはまる、と答えている。

また、共著者のLorenzoniは、このWerningの連ツイを引用しつつ以下のようにツイートしている。

I see some comments taking our paper as advocating for more inflation. This is not at all our point. Our point is that this is an inflationary shock, which is bad, and puts the Fed in an ugly spot. One thing that is sometimes hard to communicate is that the theory of optimal monetary policy tells us something about where the central bank should aim to be relative to potential output. When a shock happens that lowers potential output, the theory can tell us that we may want to be a bit above that. That is not advocating for expansionary policy, output is still going to grow less than the pre-shock trend. The slowdown in potential growth is given. Policy cannot fix that. Policy can smooth the transition and that may or not be optimal depending on the nature of the shock and of the constraints.

(拙訳)

我々の論文が、もっとインフレを、と提唱しているように解釈しているコメントを幾つか目にした。それは我々のポイントでは全くない。我々のポイントは、これはインフレ的なショックで悪いものであり、FRBを厄介な立場に追い込む、というものである。コミュニケーションが時に難しいのは、最適金融政策の理論が、潜在生産力との相対関係において中銀がどこを狙うべきか、ということに関して何かしらを伝えるものだということである。潜在生産力を低めるショックが生じると、理論は、我々がそれよりも少し上に居たいであろうということを教えてくれる。それは拡張的な政策を提唱することではない。生産は依然としてショック前のトレンドよりも低い成長に留まる。潜在生産力の鈍化は所与のものなのだ。政策がそれを直すことはできない。政策ができるのは移行を平滑化することで、それが最適か否かはショックと制約の性格に依存する。

*1:cf. Speech by Chair Powell on the economic outlook - Federal Reserve Board、情報BOX:パウエルFRB議長の講演要旨 | ロイター、パウエルFRB議長、関税の経済的影響めぐり厳しい警告 「現代にない経験」 - CNN.co.jp。

*2:cf. 仕事の階段:インフレ対再配分 - himaginary’s diary。

*3:本文では「A widely held tenet in the practice of central banking is that a shock like a tariff, that entails a mechanical increase in some prices, is a shock that requires the central bank to “see through it”. In other words, the aim is to let the mechanical price effects play out while preventing any broader ramifications. To be fair, this is a rule of thumb which, as far as we know, does not correspond to any result in economic theory.」と記述している。

*4:NBERのpdfにリンクしているので、省略。